Latest dividend announcement

South Plains Financial has declared a quarterly cash dividend of $0.17 per share. The level remains unchanged compared to the previous quarter, confirming a pause after the recent increase earlier in 2026. The dividend is payable on May 11, 2026, to shareholders of record as of April 27, 2026, with the stock trading ex-dividend on the same date.

Details of the dividend distribution

The current quarterly distribution of $0.17 translates into an annualized dividend of $0.68 per share. Based on a share price of approximately $43, the forward dividend yield stands near 1.57%. The company paid $0.16 per share in the second half of 2025 before raising the payout to $0.17 in early 2026. This step-up represents a moderate increase of 6.25% quarter-over-quarter earlier this year, followed by stabilization in the most recent declaration. The payment schedule remains consistent with a quarterly cadence, which supports predictable cash income for investors.

Relevant valuation metrics

South Plains Financial trades at a price-to-earnings ratio of 12.6 and a forward P/E of 10.2, indicating a moderate valuation relative to earnings growth expectations. The price-to-book ratio of 1.43 aligns closely with regional banking peers and reflects solid balance sheet quality. Return on equity reaches 12.5%, while return on assets stands at 1.34%, both consistent with efficient regional bank operations. The payout ratio of approximately 18% remains low, signaling substantial earnings retention capacity. Free cash flow valuation appears attractive, with a P/FCF ratio below 10, reinforcing the company’s ability to fund dividends internally without balance sheet strain. Total net income reached about $0.06 billion in 2025, supporting dividend coverage.

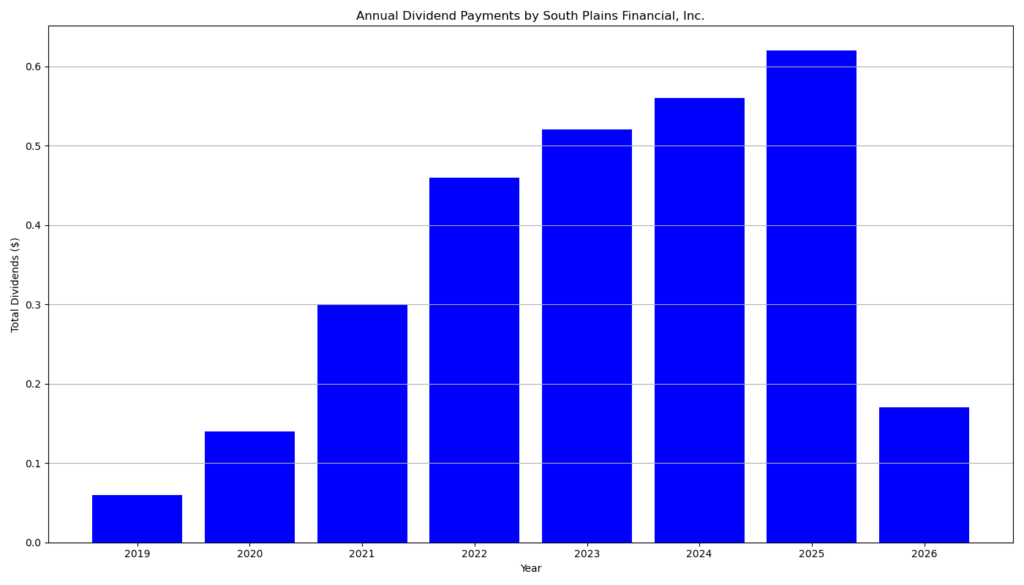

Dividend history and sustainability

South Plains Financial has established a six-year track record of uninterrupted dividend payments and growth. The dividend trajectory shows a clear upward trend from $0.03 per share in 2019 to $0.17 in 2026. Growth accelerated between 2021 and 2023, followed by more measured increases in 2024 and 2025. The latest move from $0.16 to $0.17 continues this pattern of incremental increases. The low payout ratio and consistent earnings expansion underpin dividend sustainability. The bank retains a large portion of earnings to support loan growth and capital accumulation, which reduces the risk of dividend cuts during economic downturns.

Outlook for long-term investors

South Plains Financial presents a conservative dividend profile combined with moderate growth potential. Earnings per share reached $3.44 in 2025 and are expected to increase further, with forward estimates above $4.00. Loan growth remains steady, and management targets mid-single-digit expansion supported by organic lending and strategic acquisitions. The balance sheet shows low leverage, with a debt-to-equity ratio of 0.14, and strong capital ratios above regulatory thresholds. However, the relatively low dividend yield limits immediate income appeal. The investment case therefore relies on a combination of dividend growth and capital appreciation rather than high current yield. Investors should monitor margin trends and expense discipline, as rising costs and interest rate normalization could affect profitability.

A brief company profile

South Plains Financial, Inc. operates as the holding company for City Bank, a Texas-based regional bank. The institution focuses on commercial and retail banking, complemented by mortgage, trust, and investment services. It serves small and medium-sized businesses and individuals across key Texas markets, including Dallas, Houston, and the Permian Basin, as well as parts of New Mexico. The company employs over 600 people and has grown its asset base to approximately $4.5 billion, positioning itself as a mid-sized regional banking franchise with expansion ambitions.

last quarterly report*

Here is a concise summary of the uploaded report:

Company: South Plains Financial, Inc.

Period: Q4 and Full Year 2025

Source:

Overall Performance

South Plains delivered solid full-year growth but showed slight earnings pressure in Q4.

- Full-year net income: $58.5M (↑ from $49.7M in 2024)

- Full-year EPS: $3.44 (↑ from $2.92)

- Q4 net income: $15.3M (↓ QoQ and YoY)

- Q4 EPS: $0.90 (↓ from $0.96 in prior periods)

Interpretation: The bank achieved strong annual growth, but quarterly profitability softened, indicating margin or cost pressure late in the year.

Profitability & Margins

- Net interest income (Q4): $43.0M (flat QoQ, ↑ YoY)

- Net interest margin: 4.00% (slightly ↓ QoQ, ↑ YoY)

- Return on assets (ROA): 1.36% (declining trend)

Drivers:

- Lower deposit costs supported margins.

- Falling loan yields and lower interest rates created mild pressure.

Balance Sheet & Growth

- Total assets: $4.48B (↑ from $4.23B YoY)

- Loans: $3.14B (↑ ~3% YoY)

- Deposits: $3.87B (↑ 7% YoY)

Observation: Growth is moderate and primarily organic, with stronger expansion on the deposit side.

Credit Quality

- Nonperforming assets ratio: 0.26% (stable, improved YoY)

- Net charge-offs: 0.10% (low)

- Allowance for credit losses: 1.44% of loans

Conclusion: Asset quality remains strong and stable, with no signs of systemic deterioration.

Capital & Financial Strength

- CET1 ratio: 14.45%

- Total capital ratio: 17.26%

- Tangible book value per share: $29.05 (↑ ~14% YoY)

Interpretation: Capital levels are robust and comfortably above regulatory requirements, supporting growth and acquisitions.

Expenses & Efficiency

- Noninterest expense (Q4): $33.0M (↑ YoY)

- Efficiency ratio: ~61%

Key issue: Rising operating expenses, including personnel and advisory costs, are weighing on short-term profitability.

Strategic Developments

- Acquisition of Bank of Houston (BOH) announced

- Expansion strategy focused on:

- Houston market entry

- Recruiting lenders

- Scaling operations

Management expects mid-to-high single-digit loan growth in 2026.

Dividend

- Quarterly dividend: $0.16 per share (stable QoQ)

- No increase observed in 2025

Implication: Dividend is consistent but not currently growing, suggesting a conservative capital allocation approach.

Key Takeaways

- Strong full-year earnings growth and capital generation

- Slight deterioration in Q4 profitability metrics

- Stable credit quality and improving balance sheet

- Strategic expansion could accelerate growth

- Dividend remains stable but not expanding

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 4/28/2026 After close

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.