Latest dividend announcement

Bank First Corporation has declared a quarterly cash dividend of $0.55 per share. The payment is due on July 8, 2026, to shareholders of record on June 24, 2026, with the stock trading ex-dividend on June 24. The new regular dividend is 10.0% above the prior quarterly payout of $0.50 and 22.2% above the $0.45 regular dividend paid in the year-earlier quarter. That supports the use of “increased” in the headline.

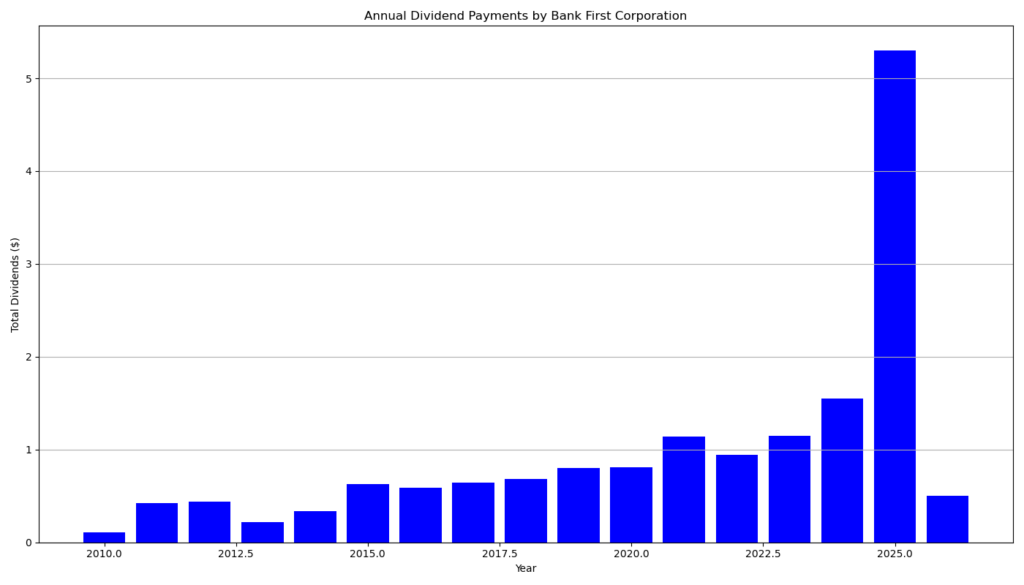

Details of the dividend distribution

On an annualized basis, the new regular payout equals $2.20 per share. Based on the share price data provided, that implies a forward yield of roughly 1.5%, which aligns with market reports published after the announcement. The distribution schedule is straightforward and consistent with Bank First’s normal quarterly cadence. For income investors, the key point is not headline yield alone. The more relevant signal is the company’s willingness to lift the regular dividend again after already moving it higher to $0.50 in March 2026.

Relevant valuation metrics

The core operating picture remains constructive. In the first quarter of 2026, Bank First reported net income of $20.0 million and GAAP EPS of $1.78. Adjusted EPS reached $2.24 after acquisition-related items. Net interest income rose to $53.2 million, and net interest margin held at 3.96%. Total assets climbed to $6.07 billion, loans reached $4.52 billion, and deposits rose to $5.09 billion, largely due to the Centre 1 Bancorp acquisition.

From a dividend-investor perspective, the valuation inputs are reasonable but not obviously cheap. The stock trades at about 20.2x trailing earnings and 13.5x forward earnings, with a price-to-book ratio of 2.22 based on the market data provided. Profitability remains healthy for a regional bank, with ROA of 1.58% and ROE of 11.09%. The balance sheet also looks conservative, with debt-to-equity of 0.19. Most important, the dividend remains well covered. The provided payout ratio is 24.9%, and even the new annualized dividend of $2.20 consumes only about 30% of trailing EPS of $7.21.

Dividend history and sustainability

The dividend record is stronger than the modest yield suggests. Bank First has posted 12 consecutive years of dividend growth and 15 consecutive years of uninterrupted dividend payments, according to the data supplied. The regular dividend moved from $0.35 in early 2024 to $0.45 through most of 2025, then to $0.50 in March 2026, and now to $0.55. That is a clear upward staircase in the ordinary payout. The company also paid a $3.50 special dividend in May 2025. Investors should separate that one-time distribution from the regular dividend trend, because including it would overstate recurring income growth.

Coverage looks sustainable, but not risk-free. Credit metrics weakened after the acquisition. Nonperforming assets increased to 0.50% of total assets from 0.20% at year-end 2025. Tangible equity to tangible assets also fell to 9.14% from 10.49%. Those figures remain manageable, but they merit monitoring.

Outlook for long-term investors

The long-term case rests on three factors: disciplined dividend growth, solid earnings power, and acquisition execution. Bank First is expanding scale while still retaining a low payout ratio. That leaves room for future dividend growth if integration proceeds as planned and credit costs stay contained. The main near-term risk is that merger-related expenses and weaker asset quality dilute returns.

A brief company profile

Bank First is a Wisconsin-based bank holding company with operations in Wisconsin and Illinois. Following the Centre transaction, it operates 38 banking locations and holds about $6 billion in assets. The franchise focuses on traditional banking, treasury management, trust, and wealth management. For dividend investors, it fits the profile of a smaller-cap bank that offers lower current yield but credible dividend compounding potential.

last quarterly report*

Bank First Corporation – Q1 2026 Summary

- Profitability:

Net income reached $20.0 million with EPS of $1.78, slightly higher than $18.2 million YoY, though EPS declined marginally. Adjusted net income was stronger at $25.1 million (EPS $2.24) due to one-time acquisition costs. - Dividend:

The company declared a quarterly dividend of $0.55 per share, representing a 10% increase QoQ and 22.2% YoY, signaling continued shareholder returns. - Growth Driver (Acquisition):

The acquisition of Centre 1 Bancorp significantly expanded scale:- Total assets rose to $6.07 billion (+33%)

- Loans increased to $4.52 billion

- Deposits grew to $5.09 billion

- Revenue & Margins:

- Net interest income: $53.2 million (strong increase QoQ and YoY)

- Net interest margin: 3.96% (slightly down QoQ, up YoY)

- Expenses & Integration Impact:

Noninterest expenses rose sharply to $39.1 million, mainly due to $6.5 million in acquisition-related costs and operational scaling. - Asset Quality:

- Nonperforming assets increased to 0.50% of total assets (from 0.20%)

- Increase driven partly by acquired loans and one large credit exposure

- Capital & Book Value:

- Equity: $819.9 million

- Book value per share: $73.05 (up from $65.47)

- Tangible book value also improved modestly

Key Takeaway:

The quarter shows strong balance sheet expansion and dividend growth driven by acquisition activity. However, integration costs and rising nonperforming assets introduce near-term pressure on profitability and risk metrics.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 7/17/2026 9:00 AM

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.