Latest dividend announcement

Eaton has declared a quarterly dividend of $1.10 per share, payable on May 29, 2026, to shareholders of record on May 8, 2026. The stock will trade ex-dividend on May 8. This announcement does not raise the payout versus the prior quarter. Eaton already lifted the quarterly rate from $1.04 to $1.10 in February 2026, so the new declaration simply confirms that higher base.

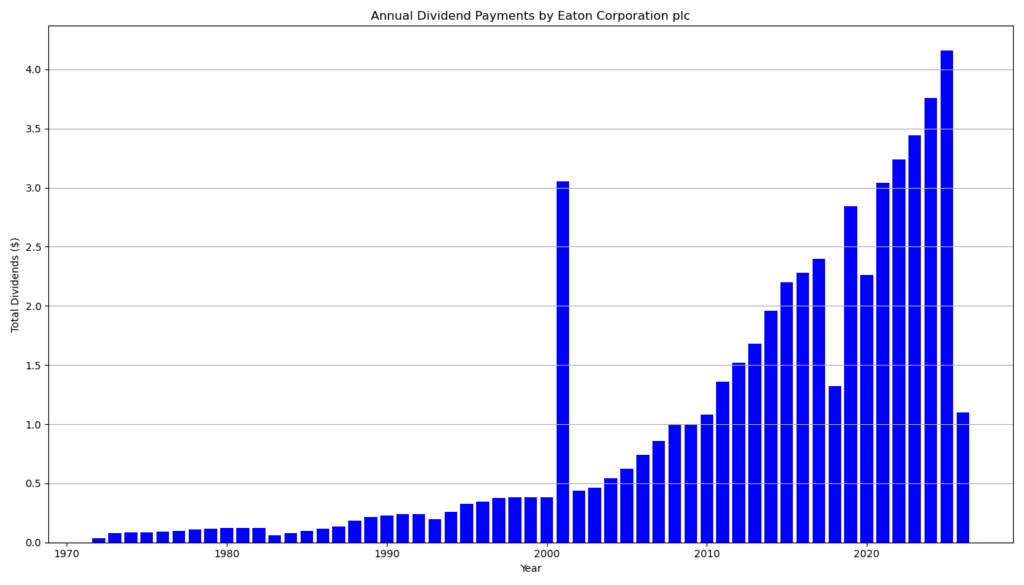

Details of the dividend distribution

The unchanged $1.10 quarterly dividend implies an annualized payout of $4.40 per share. At a recent share price of about $416.05, that translates into a forward dividend yield of roughly 1.06%, which is low for an income stock but typical for a high-multiple industrial compounder. Sequentially, the dividend is flat. Against the year-earlier quarterly rate of $1.04, however, it is up about 5.8%.

Relevant valuation metrics

For dividend investors, Eaton’s key valuation question is not headline yield but coverage quality. In 2025, the company generated $27.4 billion in revenue, $4.1 billion in net income, $10.45 in diluted EPS, $4.5 billion in operating cash flow, and $3.6 billion in free cash flow. The balance sheet ended the year with about $9.9 billion of total debt and $19.5 billion of equity. At the current market value of roughly $162.3 billion, the stock trades at about 41.6 times trailing earnings, which is a premium valuation even for a high-quality electrification franchise.

That premium only works if earnings and cash flow keep compounding. On that front, Eaton still looks fundamentally strong. Using the new annualized dividend of $4.40 and 2025 EPS of $10.45, the forward earnings payout ratio sits near 42%. That remains moderate. Free cash flow also covers the dividend comfortably. Based on 2025 diluted shares outstanding and the prior annual dividend rate of $4.16, Eaton likely paid about $1.63 billion in common dividends last year, which means 2025 free cash flow covered the cash dividend by roughly 2.2 times.

Dividend history and sustainability

Eaton has paid dividends every year since 1923. That long record matters, but investors should distinguish payment continuity from growth consistency. The recent pattern is solid. The annualized dividend rose from $3.76 in 2024 to $4.16 in 2025, and the current run rate points to $4.40 for 2026. The company also entered 2026 with favorable operating momentum after posting record 2025 EPS and record free cash flow, while guiding to 2026 EPS of $11.57 to $12.07 and adjusted EPS of $13.00 to $13.50. That earnings trajectory supports continued dividend growth, although likely at a measured pace rather than at a high-yield profile.

Outlook for long-term investors

Long-term dividend investors should view Eaton as a dividend growth name, not a current income vehicle. The investment case rests on structural exposure to electrification, grid modernization, aerospace, digitalization, and data center power demand. The risk is valuation. A yield near 1% leaves little downside protection if growth slows or if the market compresses Eaton’s multiple. Even so, Eaton’s margin profile, backlog strength, and cash generation give management room to keep raising the dividend while funding acquisitions and capital expenditure. The next checkpoint arrives with first-quarter 2026 earnings on May 5.

A brief company profile

Eaton is an intelligent power management company founded in 1911. It serves data center, utility, industrial, commercial, residential, aerospace, and mobility end markets. The company operates globally and generated $27.4 billion in 2025 revenue. Its business mix gives it direct exposure to several long-duration capital investment cycles that matter for dividend durability. For investors who prioritize payout resilience over headline yield, that profile remains attractive.

last quarterly report*

Here is a concise summary of the uploaded Eaton 2025 earnings report:

Financial performance (2025):

- Revenue: $27.4 billion, up 10% YoY

- Net income: $4.1 billion, up from $3.8 billion

- EPS: $10.45, up 10% YoY

- Adjusted EPS: $12.07, up 12% YoY

Q4 2025 highlights:

- Sales: $7.1 billion, up 13% YoY

- EPS: $2.91 (adjusted: $3.33), both record levels

- Free cash flow: $1.6 billion, up 17% YoY

- Segment margin: 24.9%, record high

Cash flow (full year):

- Operating cash flow: $4.5 billion

- Free cash flow: $3.6 billion (slightly up YoY)

Growth drivers:

- Strong demand in Electrical Americas (+21% Q4 sales)

- Solid Aerospace growth (+14% Q4 sales)

- Backlog growth: +29% Electrical, +16% Aerospace

- Book-to-bill ratio: 1.1, indicating continued demand momentum

Balance sheet:

- Total debt: ~$9.9 billion

- Equity: $19.5 billion

- Assets: $41.3 billion

Outlook (2026):

- EPS guidance: $11.57–$12.07 (~13% growth midpoint)

- Adjusted EPS: $13.00–$13.50

- المتوقع organic growth: 7–9%

Strategic developments:

- Continued acquisitions (e.g., Fibrebond, Ultra PCS)

- Planned Mobility business spin-off by 2027

- Strong exposure to megatrends: electrification, AI, data centers

Bottom line:

Eaton delivered record profitability, strong margin expansion, and robust order momentum. Growth is driven by electrification and aerospace demand, while backlog and guidance suggest continued earnings expansion into 2026.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 5/1/2026 6:00 AM

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.