Latest Dividend Announcement

Turning Point Brands, Inc. (NYSE: TPB) has declared a quarterly dividend of $0.08 per common share. This represents a 7% increase compared to the previous quarterly dividend of $0.075 paid in December 2025. The company has now raised its dividend for eight consecutive years, reinforcing its capital return policy and signaling continued confidence in cash flow generation.

Details of the Dividend Distribution

The dividend is payable on April 10, 2026, to shareholders of record as of March 20, 2026. The ex-dividend date is March 20, 2026. On an annualized basis, the new payout amounts to $0.32 per share. Based on the current share price of $144.38, the forward dividend yield stands at approximately 0.22%. While the yield remains modest, the company prioritizes dividend growth over high current income.

Turning Point Brands operates with a conservative payout ratio of approximately 9%. This low distribution ratio leaves substantial headroom for reinvestment, debt service, acquisitions, and further dividend increases.

Relevant Valuation Metrics

Turning Point Brands currently has a market capitalization of roughly $2.75 billion and an enterprise value of approximately $2.85 billion. The stock trades at a forward price-to-earnings ratio of about 35x, based on forward earnings per share of $4.13. The trailing P/E stands higher at 44x, reflecting recent earnings acceleration.

Revenue totals approximately $435.7 million, with year-over-year growth of 31%. EBITDA reaches about $108.7 million, translating into an EBITDA margin of 24.9%. The enterprise value-to-EBITDA multiple of 26x indicates a premium valuation relative to traditional tobacco peers, justified by higher growth in modern oral and alternative product categories.

Free cash flow amounts to approximately $38.1 million. Given the annual dividend obligation of roughly $6 million, free cash flow covers the dividend multiple times over. The balance sheet shows total cash of about $201.2 million against total debt of approximately $307.2 million, resulting in moderate net leverage. The price-to-book ratio of 8.0 reflects strong market expectations for continued earnings expansion.

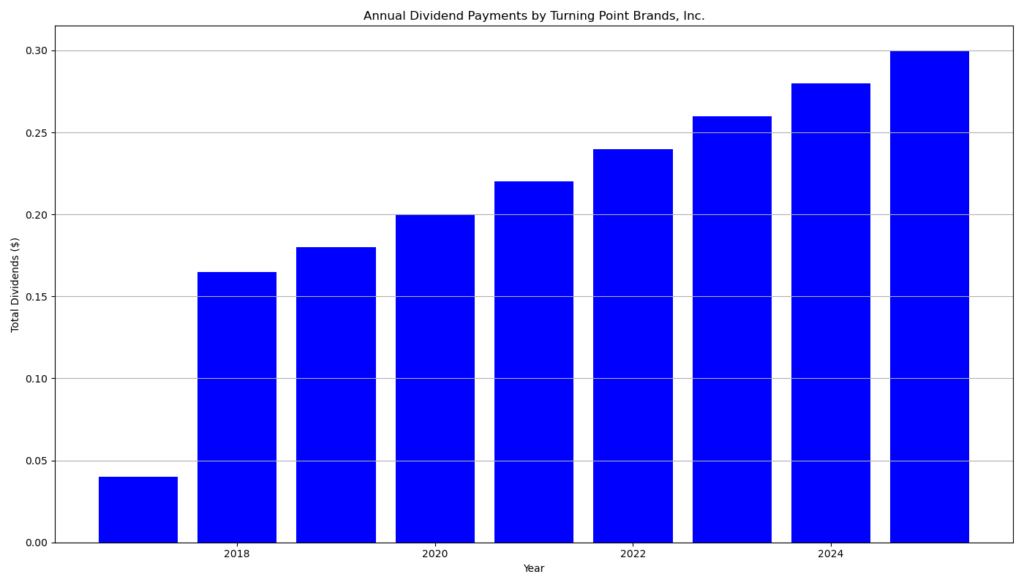

Dividend History and Sustainability

Turning Point Brands initiated quarterly dividends at $0.04 in 2017. The company steadily increased the payout to $0.045 in 2018, $0.05 in 2020, $0.055 in 2021, $0.06 in 2022, $0.065 in 2023, $0.07 in 2024, and $0.075 in 2025. The newly declared $0.08 dividend marks the eighth consecutive year of growth and the eighth uninterrupted year of payments.

The compound annual growth rate since 2017 exceeds 9%. Importantly, management funds these increases from operating earnings rather than excessive leverage. With earnings growth of nearly 69% year over year and quarterly earnings growth above 70%, dividend coverage remains robust. The low payout ratio provides a strong margin of safety even under cyclical pressure.

Outlook for Long-Term Investors

Turning Point Brands combines moderate leverage, high EBITDA margins, and strong earnings momentum. The company operates in a defensive sector but benefits from structural growth in alternative smoking accessories and modern oral nicotine products. Its beta of 0.88 suggests lower volatility than the broader market.

The valuation multiple appears elevated. However, investors price in sustained double-digit earnings growth and expanding margins. Long-term dividend investors should focus on the company’s disciplined payout strategy, strong free cash flow conversion, and expanding product portfolio. If earnings growth moderates, the low payout ratio will still support continued dividend increases.

A Brief Company Profile

Turning Point Brands, Inc., headquartered in Louisville, Kentucky, manufactures, markets, and distributes branded consumer products in the tobacco and alternative smoking accessories industry. Its portfolio includes Zig-Zag®, Stoker’s®, FRE®, and ALP®. The company distributes products through more than 220,000 retail outlets across North America and through direct-to-consumer channels. It operates within the Consumer Defensive sector and competes in the evolving tobacco and modern oral product markets.

last quarterly report*

Turning Point Brands, Inc. – Form 10-Q Summary (Quarter Ended September 30, 2025)

Revenue and Profitability

Turning Point Brands reported strong top-line growth in both the third quarter and the first nine months of 2025.

For the three months ended September 30, 2025, net sales increased 31.2% to $118.98 million, compared to $90.70 million in the prior-year period . Growth was driven primarily by the Stoker’s segment, while Zig-Zag products declined year over year .

Operating income rose to $25.89 million from $20.81 million . Net income attributable to Turning Point Brands increased to $21.08 million, up from $12.38 million in the prior year . Diluted EPS improved significantly to $1.13 versus $0.68 in Q3 2024 .

For the nine-month period, net sales increased 28.1% to $342.05 million, compared to $266.99 million in 2024 . Net income attributable to the company reached $49.96 million, up from $37.39 million . Diluted EPS rose to $2.70 from $1.99 .

Segment Performance

Stoker’s products drove most of the growth. In Q3, Stoker’s net sales increased 80.8% year over year, while Zig-Zag sales declined 10.5% . For the nine months, Stoker’s sales rose 69.0%, whereas Zig-Zag sales fell 5.5% .

This mix shift toward Stoker’s materially influenced overall profitability. However, corporate unallocated expenses increased, partly due to joint venture-related costs .

Capital Structure and Debt

As of September 30, 2025, total gross long-term debt stood at $300.0 million, reflecting the issuance of 7.625% Senior Secured Notes due 2032 . Net debt (after deferred finance costs) totaled $293.36 million .

The company redeemed its 2026 Notes using proceeds from the new issuance . Interest expense for the nine-month period increased to $13.09 million from $10.35 million in the prior year .

Importantly, the company had no borrowings outstanding under its 2023 ABL Facility as of quarter-end and retained $66.6 million in availability .

Liquidity Position

Cash on hand totaled $201.2 million at September 30, 2025 . Management stated that liquidity remains strong, supported by cash balances, free cash flow generation, and ABL availability .

Adjusted working capital increased due to higher receivables, inventory, and other current assets .

Equity and Capital Allocation

During the quarter, the company raised approximately $97.5 million in net proceeds through its at-the-market (ATM) equity program .

As of September 30, 2025, stockholders’ equity totaled $358.15 million, up from $190.38 million at year-end 2024 .

The company continues to pay a quarterly dividend. However, dividend payments qualify as restricted payments under the 2032 Notes indenture and are subject to covenant limitations .

Overall Assessment

Turning Point Brands delivered strong revenue and earnings growth in Q3 and year-to-date 2025, largely driven by the Stoker’s segment. Profitability improved materially, and EPS growth outpaced revenue growth.

The company strengthened liquidity through both debt refinancing and equity issuance. While leverage remains significant at $300 million in senior secured notes, the substantial cash balance and undrawn credit facility provide financial flexibility.

Key considerations going forward include sustained growth in Stoker’s, continued weakness in Zig-Zag, regulatory risks, and the higher interest burden from the 7.625% notes issuance.

*This is the latest quarterly report that the company has filed with the SEC.

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?