Latest dividend announcement

Casey’s General Stores has declared a quarterly dividend of $0.57 per share, maintaining the same payout as the previous quarter. The board confirmed the distribution on March 10, 2026. At the current share price of approximately $678, the dividend corresponds to a forward annual payout of $2.28 per share and a forward dividend yield of about 0.34%.

The company has developed a reputation for consistent shareholder returns. However, the latest declaration does not represent an increase compared with the previous quarter. Casey’s last raised its quarterly dividend in August 2025, when the payout rose from $0.50 to $0.57 per share.

Details of the dividend distribution

The dividend will be paid on May 15, 2026. Shareholders must be on record as of May 1, 2026, which also marks the ex-dividend date. Investors purchasing the stock on or after that date will not receive the upcoming distribution.

On an annualized basis, Casey’s distributes $2.28 per share in dividends. Despite the modest yield, the company emphasizes capital appreciation and reinvestment in expansion projects. Management typically balances dividend growth with store development, acquisitions, and share repurchases.

The payout ratio remains conservative. Based on a forward earnings estimate of about $19.44 per share, the implied payout ratio stands near 13%, indicating a substantial margin of safety for dividend sustainability.

Relevant valuation metrics

Casey’s operates with solid financial fundamentals that support its dividend policy. The company currently carries a market capitalization of roughly $25 billion and an enterprise value of approximately $27 billion.

The stock trades at a forward price-to-earnings ratio of about 34.9, reflecting strong earnings growth expectations and the market’s confidence in the company’s expansion strategy. Analysts expect significant profit momentum, supported by an earnings growth rate approaching 50% year over year.

Profitability metrics remain stable. Casey’s generates EBITDA of about $1.39 billion, which translates into an EBITDA margin of roughly 8.2%. The company also produced free cash flow of approximately $461 million, providing additional capacity for dividends, debt reduction, and capital expenditures.

Balance sheet leverage remains moderate. Casey’s holds around $465 million in cash while carrying total debt of about $2.9 billion. This capital structure allows the company to fund expansion while maintaining a conservative dividend payout.

Dividend history and sustainability

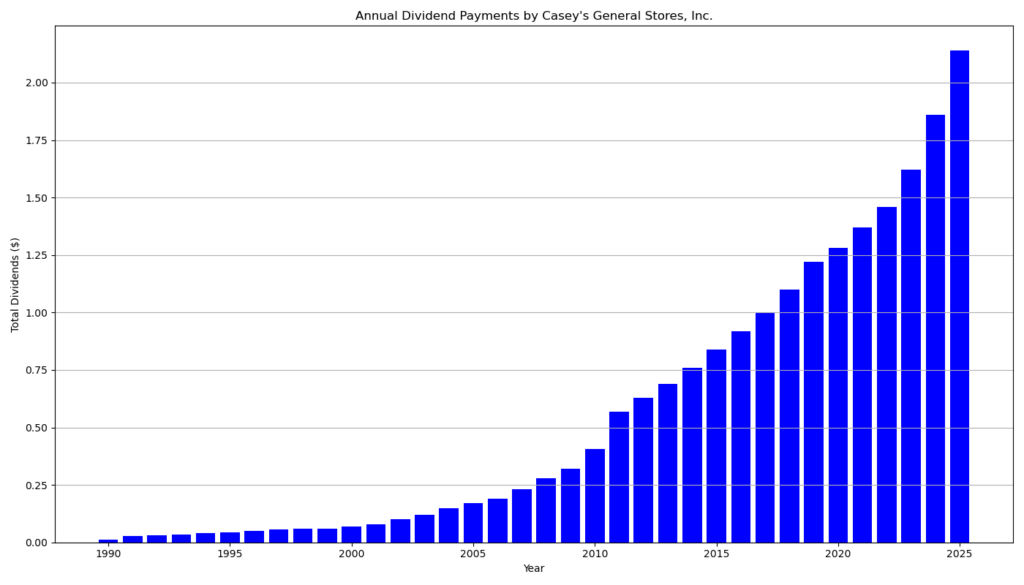

Casey’s has built one of the longest dividend growth records in the retail convenience store sector. The company has delivered 36 consecutive years of dividend increases and 35 consecutive years of uninterrupted dividend payments.

The long-term dividend trajectory demonstrates steady growth. Quarterly dividends measured $0.10 per share in 2010, increased to $0.32 by 2019, and rose further to $0.43 in 2023. The most recent increase occurred in 2025, when the payout climbed from $0.50 to $0.57 per quarter.

Such a record reflects a disciplined capital allocation strategy. The low payout ratio allows management to sustain dividend growth even during periods of economic volatility.

Outlook for long-term investors

Casey’s growth strategy focuses on expanding its convenience store footprint, increasing prepared food sales, and improving operating margins. The company continues to invest heavily in store construction and acquisitions across the Midwestern United States.

The business also benefits from strong demand in the prepared food segment, particularly pizza and hot food offerings, which carry higher margins than fuel sales. These operational advantages support earnings growth and provide a solid foundation for future dividend increases.

For long-term investors, Casey’s represents a growth-oriented dividend stock rather than a high-yield income vehicle. The combination of steady dividend increases, strong earnings growth, and ongoing expansion creates a compelling long-term investment profile.

A brief company profile

Casey’s General Stores, Inc., headquartered in Ankeny, Iowa, operates one of the largest convenience store chains in the United States. The company manages nearly 3,000 locations across several Midwestern and Southern states.

Its stores offer fuel, grocery items, and a broad prepared food menu, including the brand’s well-known fresh pizza program. With annual revenue of nearly $17 billion, Casey’s ranks among the leading operators in the specialty retail and convenience store industry.

The company’s strategy combines organic store development with targeted acquisitions. This approach continues to expand Casey’s geographic presence while strengthening its long-term earnings and dividend growth potential.

last quarterly report*

Casey’s General Stores Q3 FY2026 earnings release.

Key Results (Q3 FY2026)

- Diluted EPS: $3.49, up 49.8% YoY

- Net income: $130.1 million, up 49.3% YoY

- EBITDA: $308.9 million, up 27.5% YoY

The strong profit growth was mainly driven by higher gross profit in both inside sales and fuel, partly offset by higher operating expenses.

Revenue and Sales Performance

- Total revenue: $3.92 billion (roughly flat YoY)

- Inside sales: $1.48 billion, +5.7% YoY

- Inside same-store sales: +4.0%

- Inside gross margin: 42.2%, up from 40.9%

Prepared food and beverages (especially pizza and hot sandwiches) and non-alcoholic beverages were key drivers of same-store growth.

Fuel Business

- Fuel gallons sold: 848 million gallons (+2.3% YoY)

- Same-store fuel gallons: +0.4%

- Fuel gross profit: $348.2 million (+15.3% YoY)

- Fuel margin: 41.0 cents per gallon (vs. 36.4 cents last year)

Higher margins and slightly higher volumes drove fuel profit growth.

Expenses

- Operating expenses: $697.6 million (+4.1% YoY)

Key drivers:

- higher labor costs

- additional store locations

- weather-related snow removal costs

- higher incentive compensation accruals

Cash Flow and Balance Sheet

- Operating cash flow (9 months): $979 million

- Cash and equivalents: $465 million

- Available liquidity: about $1.4 billion (cash + credit facilities)

The company also repurchased $76 million of shares during the quarter.

Store Expansion

- Store count: 2,924 locations as of Jan 31, 2026

- Net increase driven by 27 new builds and 27 acquisitions, partly offset by closures/divestitures.

Dividend

- Quarterly dividend: $0.57 per share

- Payment date: May 15, 2026

- Record date: May 1, 2026

Fiscal 2026 Outlook

Management expects:

- EBITDA growth: +18% to +20% for FY2026

- Inside same-store sales growth: 3.5%–4.5%

- Operating expense growth: about 10%

- Planned store openings: at least 80 during FY2026

Overall Assessment

Casey’s delivered very strong earnings growth despite flat revenue, mainly through:

- higher margins

- operational efficiency

- growth in prepared food sales

- stronger fuel profitability.

The company continues to expand its store network and loyalty program (which surpassed 10 million members), supporting long-term growth.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 6/8/2026 After close

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?