Latest dividend announcement

Howmet Aerospace has declared a quarterly dividend of $0.12 per share. The new distribution is in line with the previous quarter, so this is not a fresh increase. The board approved the payment for May 26, 2026, with a record date of May 8, 2026 and the stock trading ex-dividend on May 8, 2026.

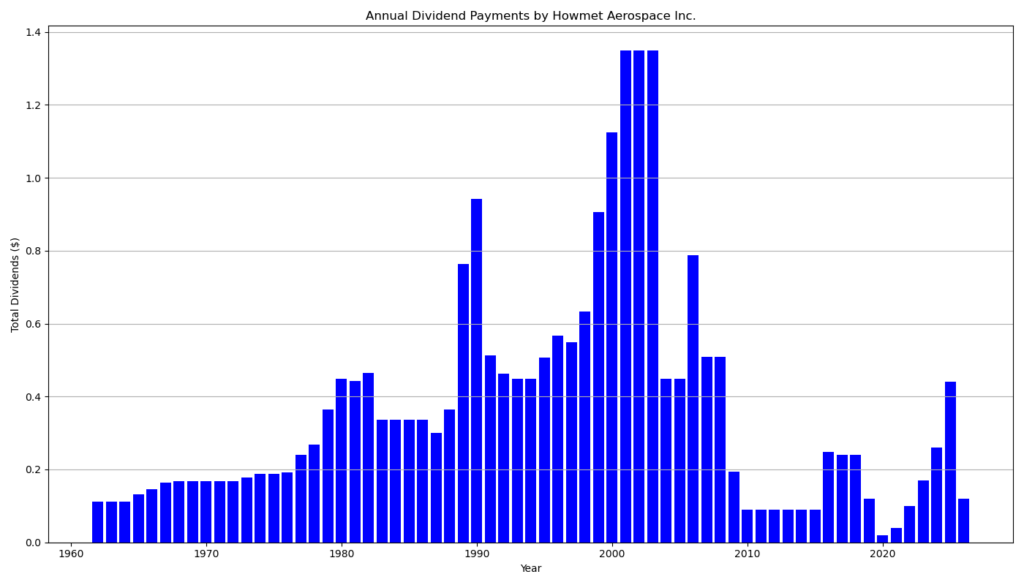

Details of the dividend distribution

The flat quarterly rate matters because Howmet raised the dividend twice in 2025 and has now paused at the new level. The company paid $0.10 in May 2025, then lifted the quarterly payout to $0.12 in August 2025. It maintained that level for the November 2025, February 2026, and now May 2026 distributions. That means the latest declaration matches the prior payment exactly, but still stands 20% above the first-quarter 2025 rate of $0.10 and 50% above the fourth-quarter 2024 rate of $0.08. The annualized run rate is $0.48 per share.

Relevant valuation metrics

Howmet remains a low-yield, high-growth industrial compounder rather than a traditional income stock. The indicated dividend yield sits near 0.2%, which keeps income modest at the current share price. The more relevant metrics for long-term dividend investors sit below the yield line. The stock carries a payout ratio of 11.86%, which leaves substantial headroom for future increases. Profitability is also strong. Return on equity stands at 30.44%, return on invested capital at 18.07%, operating margin at 25.81%, and net margin at 18.25%. Those figures indicate a business with high incremental returns and strong pricing power in aerospace components.

Valuation looks demanding. Shares trade at roughly 67.6x trailing earnings, 45.1x forward earnings, and about 70.3x free cash flow based on the supplied market data. That premium reflects strong operating execution and multi-year aerospace demand, but it also compresses the current yield and raises the execution bar for new investors.

Dividend history and sustainability

The dividend record is stronger than the headline yield suggests. Howmet has logged 26 consecutive years of dividend payments and five consecutive years of dividend growth based on the supplied history. The record is not perfectly linear over longer periods, however. The historical table shows several resets and reductions before the current growth phase. Investors should therefore frame the recent dividend acceleration as a recovery and expansion cycle, not as an uninterrupted multi-decade growth streak.

Coverage looks robust. In full-year 2025, Howmet generated $1.43 billion of free cash flow on $1.51 billion of net income, with free-cash-flow conversion near 93% of net income excluding special items. The company paid $181 million in common dividends during 2025, which implies ample cash coverage. Balance-sheet risk also looks manageable. Year-end cash stood near $0.74 billion, while long-term debt declined to about $2.86 billion after debt reduction actions in 2025.

Outlook for long-term investors

The investment case rests on earnings growth and capital discipline, not on immediate income. Management guided for about $9.0 billion to $9.2 billion in 2026 revenue, adjusted EPS of $4.35 to $4.55, and free cash flow of $1.55 billion to $1.65 billion. If Howmet sustains that trajectory, the dividend should retain significant growth capacity even after the recent step-up. The main risk is valuation. A premium multiple limits margin of safety, especially in a cyclical aerospace supply chain. Still, the combination of low payout, strong free cash flow, and expanding margins gives the dividend a solid technical foundation.

A brief company profile

Howmet Aerospace, headquartered in Pittsburgh, supplies highly engineered components for aerospace, defense, gas turbines, and commercial transportation. Its core businesses include engine products, fastening systems, structural components, and forged wheels. The company benefits from long-cycle aerospace demand, high certification barriers, and a large installed base that supports recurring aftermarket and replacement demand.

last quarterly report*

Here is a concise summary of the report:

Company: Howmet Aerospace

Period: Q4 and Full Year 2025

Source:

Key Financial Performance

- Revenue

- Q4 2025: $2.2B (+15% YoY)

- FY 2025: $8.3B (+11% YoY)

Growth driven primarily by commercial and defense aerospace.

- Profitability

- Q4 net income: $372M (EPS $0.92, +19% YoY)

- FY net income: $1.5B (EPS $3.71 vs. $2.81 prior year)

- Adjusted EPS grew faster (+40% YoY for full year), indicating margin expansion.

- Margins

- FY operating margin: 24.8% (up 280 bps)

- Adjusted EBITDA margin: ~29–30%, showing strong operating leverage.

Cash Flow and Capital Allocation

- Free cash flow (FY 2025): ~$1.4B

- Cash from operations: $1.9B

- High conversion: ~93% of net income → strong earnings quality

- Capital deployment:

- Share buybacks: $700M

- Dividends paid: $181M

- Debt reduction: $265M

Dividend

- Quarterly dividend: $0.12 per share

- Growth:

- +50% YoY vs. Q4 2024 ($0.08)

- +20% vs. Q1 2025 ($0.10)

This indicates an aggressive dividend growth phase, though the absolute yield remains modest.

Balance Sheet

- Total debt reduced (net): improved structure

- Long-term debt: $2.86B (down from $3.31B)

- Cash: $742M

- Pension liabilities reduced

Overall: deleveraging trend + improving financial flexibility

Business Segment Highlights

- Engine Products (core segment):

- Strongest growth (+16% FY revenue)

- EBITDA margin ~33%

- Fastening Systems:

- Margin expansion to ~30%

- Engineered Structures:

- Highest margin improvement (+560 bps)

- Forged Wheels:

- Weak demand in commercial transportation, but margins stabilized

Strategic Moves

- Acquisition of CAM (~$1.8B) to expand aerospace fasteners

- Smaller bolt-on acquisition (Brunner)

- Continued aggressive share repurchases

2026 Outlook

- Revenue guidance: ~$9.0–9.2B (~+10%)

- EPS guidance: $4.35–4.55

- Free cash flow: $1.55–1.65B

Management expects continued growth + margin expansion

Interpretation (Dividend Investor Perspective)

- Strengths:

- Strong free cash flow generation

- High FCF conversion → supports dividends

- Rapid dividend growth

- Improving margins and balance sheet

- Limitations:

- Dividend yield still relatively low

- Capital allocation heavily skewed toward buybacks

- Cyclical exposure to aerospace markets

Bottom Line

Howmet delivered record revenue, earnings, and cash flow in 2025, supported by aerospace demand. The company is transitioning into a high-margin, cash-generative industrial compounder, with increasing dividend capacity, though it currently prioritizes share repurchases over yield-focused income distribution.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 5/7/2026 7:00 AM

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.