Latest dividend announcement

Morgan Stanley declared a quarterly dividend of $1.00 per share for the second quarter of 2026. The payout remains unchanged compared to the previous quarter, confirming a stable distribution policy. The forward dividend yield stands at approximately 2.18%, positioning the stock in line with large-cap financial peers.

Details of the dividend distribution

The dividend will be paid on May 15, 2026, to shareholders of record as of April 30, 2026. The ex-dividend date is also April 30, 2026. On an annualized basis, the current distribution amounts to $4.00 per share, slightly above the trailing twelve-month dividend of $3.92 due to the mid-2025 increase. The unchanged quarterly level indicates that management currently prioritizes consistency over incremental increases following last year’s adjustment from $0.925 to $1.00 per share.

Relevant valuation metrics

Morgan Stanley exhibits solid profitability and moderate valuation levels. The stock trades at a forward P/E ratio of 15.5, below the broader market multiple of 18.9, suggesting a relative valuation discount. Earnings per share reached $10.21 on a trailing basis and are expected to rise to $12.42 next year, implying continued earnings growth.

From a dividend perspective, the payout ratio of 37.7% remains conservative for a financial institution. This level provides a significant buffer for both reinvestment and future dividend increases. The price-to-book ratio of 2.99 reflects strong returns on equity, which stand at approximately 15.6%. In addition, the company reported a return on tangible common equity above 27% in the latest quarter, underlining high capital efficiency.

The combination of earnings growth, moderate valuation, and a disciplined payout ratio supports the sustainability of the current dividend yield.

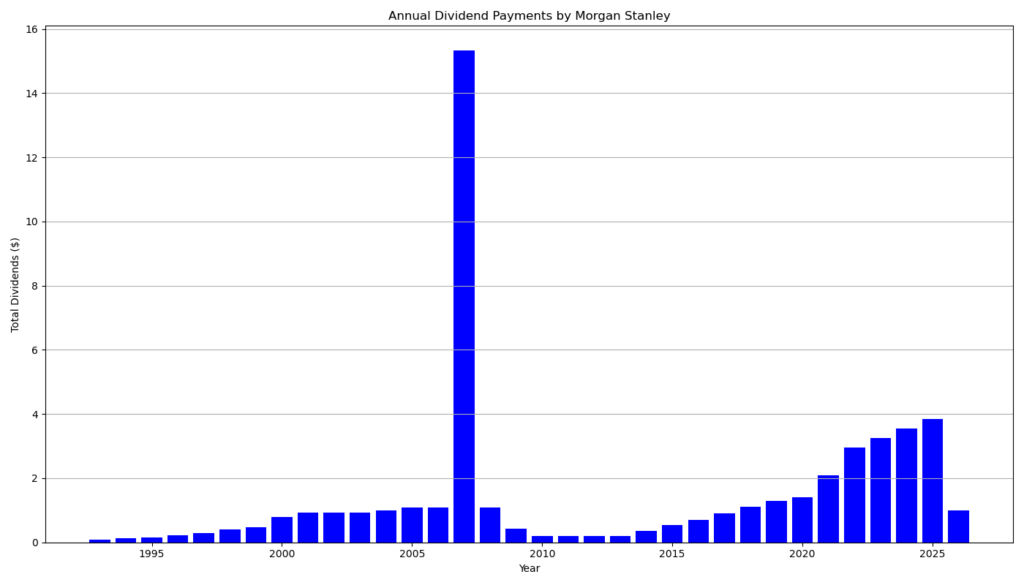

Dividend history and sustainability

Morgan Stanley has established a robust dividend track record. The company has paid dividends for 28 consecutive years and increased its payout for 12 consecutive years. This consistency reflects a structurally improved business model following the global financial crisis.

Dividend growth has accelerated in recent years. The quarterly payout increased from $0.70 in 2021 to $1.00 in 2025, representing substantial cumulative growth. The most recent increase occurred in mid-2025, when the dividend rose by approximately 8%. Since then, the company has maintained the higher level.

The sustainability of the dividend remains supported by strong earnings momentum. Net income reached approximately $5.6 billion in the first quarter of 2026, while capital ratios remain robust with a CET1 ratio above 15%. These metrics indicate that the current payout is well covered by both earnings and regulatory capital buffers.

Outlook for long-term investors

Morgan Stanley benefits from a diversified revenue mix across investment banking, trading, and wealth management. The wealth management segment, in particular, provides stable fee-based income and supports predictable cash flows. This stability is critical for dividend investors.

Looking ahead, analysts expect mid- to high-single-digit EPS growth over the next several years. Combined with a conservative payout ratio, this creates room for continued dividend growth. However, the absence of a recent increase suggests that management may adopt a more measured pace of capital returns in the near term.

The stock’s strong price performance, with gains exceeding 70% over the past year, has compressed the dividend yield slightly. Nevertheless, the combination of capital appreciation, earnings growth, and reliable income continues to offer an attractive total return profile.

A brief company profile

Morgan Stanley is a leading global financial services firm headquartered in New York. The company operates across investment banking, institutional securities, wealth management, and investment management. It serves corporations, governments, institutions, and private clients worldwide. With approximately 83,000 employees and a market capitalization exceeding $300 billion, Morgan Stanley ranks among the most significant U.S. financial institutions.

last quarterly report*

Here is a concise summary of Morgan Stanley’s Q1 2026 results:

Overall performance

- Record quarter with net revenue of $20.6B (+16% YoY) and net income of $5.6B (+29% YoY)

- EPS: $3.43 (vs. $2.60 last year)

- Strong profitability with ROTCE of 27.1% and ROE of 21%

Business segments

- Institutional Securities:

- Revenue: $10.7B (+19% YoY)

- Growth driven by investment banking (+36%), equities (+25%), and fixed income (+29%)

- Wealth Management:

- Revenue: $8.5B (+16% YoY), record level

- Strong inflows: $118B net new assets and $54B fee-based flows

- Investment Management:

- Revenue: $1.5B (−4% YoY)

- Decline due to lower performance-based income

Profitability & efficiency

- Pre-tax income: $7.0B (+26% YoY)

- Expense efficiency ratio: improved to 65% (from 68%)

- Margin expansion reflects operating leverage despite higher compensation costs

Balance sheet & capital

- CET1 ratio: 15.1% (solid capital position)

- Total assets: ~$1.58T (+22% YoY)

- Continued capital return: $1.75B share buybacks

Dividend

- Quarterly dividend: $1.00 per share

Key takeaways for investors

- Strong earnings growth and high returns on capital indicate excellent profitability

- Wealth Management remains the core growth and stability driver

- Capital levels and buybacks support shareholder returns

- Slight weakness in Investment Management is a minor offset

Bottom line:

Morgan Stanley delivered a high-quality quarter with broad-based growth, strong margins, and robust capital return—particularly attractive for long-term and dividend-focused investors.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date:

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.