Latest dividend announcement

National Fuel Gas Company announced a regular quarterly dividend of $0.535 per share, maintaining the previous payout level. The board of directors approved the distribution on March 12, 2026. The dividend remains unchanged compared with the prior quarter, when the company also paid $0.535 per share. At the current share price of about $93.93, the distribution corresponds to a forward dividend yield of roughly 2.3%.

The stable payout reflects the company’s long-standing dividend policy, which prioritizes predictable income streams and gradual annual increases rather than frequent quarterly adjustments.

Details of the dividend distribution

National Fuel Gas will distribute the dividend on April 15, 2026. Shareholders must hold the stock by the record date of March 31, 2026, which also marks the ex-dividend date. Only investors listed in the company’s shareholder registry at the close of business on that date will receive the payment.

The company has approximately 95 million shares outstanding, implying a total quarterly cash distribution of roughly $50.8 million to shareholders. On an annualized basis, the dividend amounts to about $2.14 per share, resulting in total annual dividend payments of approximately $0.20 billion.

Relevant valuation metrics

National Fuel Gas operates in the integrated oil and gas sector and currently carries a market capitalization of about $8.9 billion. The stock trades at a forward price-to-earnings ratio of approximately 11.3, based on expected earnings per share of about $8.33. The trailing P/E ratio stands near 13.1, which places the valuation below the broader energy sector average.

The company reports enterprise value of roughly $11.3 billion, with an EV/EBITDA multiple of about 7.5. EBITDA recently reached approximately $1.5 billion, indicating solid operating profitability.

From an income-investor perspective, the most relevant metric remains the payout ratio of roughly 29.6%. This relatively conservative distribution ratio suggests that National Fuel Gas retains significant earnings to finance capital expenditures and infrastructure expansion while maintaining dividend stability.

The balance sheet also remains manageable. Total debt amounts to about $2.8 billion, while the company holds more than $0.27 billion in cash.

Dividend history and sustainability

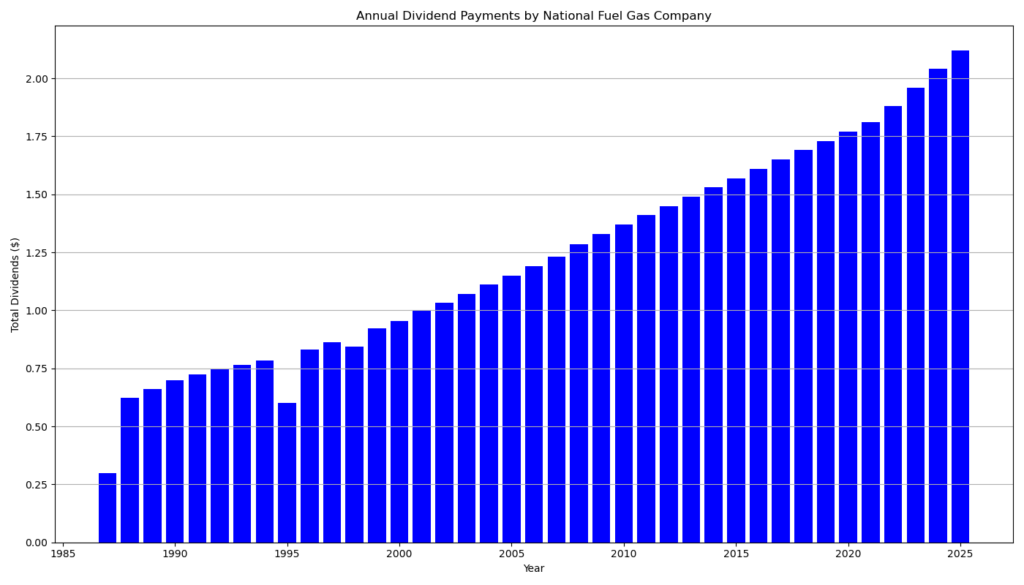

National Fuel Gas stands among the most consistent dividend payers in the U.S. energy sector. The company has delivered 54 consecutive years of dividend growth and the same number of uninterrupted annual dividend payments. This track record places it among the Dividend Aristocrats of the energy industry.

The historical dividend series shows gradual but steady increases over decades. Quarterly payments amounted to $0.150 per share in the late 1980s. The payout rose steadily through the 1990s and 2000s and reached $0.495 in 2023. The most recent annual increase occurred in 2025, when the dividend rose from $0.515 to $0.535 per share.

The combination of moderate payout ratios, stable regulated utility cash flows, and diversified upstream gas production supports the sustainability of this dividend policy.

Outlook for long-term investors

National Fuel Gas continues to invest heavily in natural gas development, pipeline infrastructure, and regulated utility operations. These segments generate relatively stable cash flows that support the company’s dividend strategy.

The stock’s valuation multiples remain moderate compared with peers. A forward P/E near 11 and EV/EBITDA below 8 suggest that the market prices the company conservatively despite its long dividend track record.

For income-oriented investors, the combination of consistent dividend growth, moderate payout ratios, and defensive utility earnings creates an attractive long-term profile. However, the yield remains modest compared with other energy infrastructure companies. Future dividend growth will likely depend on natural gas prices, capital expenditure efficiency, and regulatory developments in its utility operations.

A brief company profile

National Fuel Gas Company is a diversified energy enterprise headquartered in Williamsville, New York. The company operates across three primary segments: natural gas exploration and production, pipeline and storage infrastructure, and regulated natural gas utilities.

Its upstream subsidiary Seneca Resources focuses on the Appalachian Basin, particularly in Pennsylvania. The pipeline and storage business operates an integrated network of transportation and storage facilities across New York and Pennsylvania. The utility segment serves residential, commercial, and industrial customers in the northeastern United States.

This integrated structure provides both commodity exposure and regulated earnings streams, which together support the company’s long-standing dividend policy.

last quarterly report*

Overview

National Fuel Gas reported strong first-quarter fiscal 2026 results, driven mainly by higher natural gas production and improved realized gas prices. Adjusted earnings grew significantly year over year, while the company maintained its full-year guidance.

The report can be accessed here:

Key Financial Results (Q1 FY2026)

Earnings

- Net income: $181.6 million

- Diluted EPS: $1.98

- Adjusted EPS: $2.06

In the same quarter last year:

- Net income: $45.0 million

- EPS: $0.49

- Adjusted EPS: $1.66

The large jump in GAAP earnings partly reflects impairment charges recorded in the prior year, which distort the year-over-year comparison. On an adjusted basis, EPS increased about 24%.

Revenue and Operations

Total operating revenue rose to $651.5 million, up from $549.5 million a year earlier.

Growth came primarily from the Integrated Upstream and Gathering segment, which benefited from:

- Higher production volumes

- Improved natural gas prices

- Strong drilling results in the Utica formation in Tioga County

Natural gas production reached 109 Bcf, an increase of 12% year-over-year.

Realized prices after hedging rose to $2.89 per Mcf, up 14%.

Segment Performance

Integrated Upstream & Gathering

- Adjusted earnings: $124.0 million

- Adjusted EBITDA: $268.4 million

This segment delivered the strongest growth due to higher gas production and prices.

Pipeline & Storage

- Net income: $31.2 million

- Slight decline from the previous year because of lower other income.

Utility

- Net income: $34.1 million

- Earnings increased 5% year-over-year.

Growth in the utility segment came mainly from:

- Higher customer margins

- Colder winter weather

- Rate increases in New York.

Cash Flow and Investment

- Operating cash flow: $274.9 million

- Capital expenditures: $277.6 million

- Cash balance: $271.4 million at quarter end.

The company continues to invest heavily in:

- Natural gas development

- Pipeline infrastructure

- Utility system modernization.

Strategic Developments

Important corporate developments during the quarter include:

- $350 million equity issuance to fund a pending acquisition.

- Planned acquisition of CenterPoint Energy’s Ohio natural gas utility, expected to close in late 2026.

- Continued progress on two pipeline expansion projects:

- Tioga Pathway

- Shippingport Lateral

Both projects remain on track for service in late 2026.

Outlook

National Fuel reaffirmed fiscal 2026 guidance:

- Adjusted EPS: $7.60–$8.10

- Midpoint: $7.85 per share.

Guidance assumes an average NYMEX natural gas price of $3.75/MMBtu for the remainder of the fiscal year.

The upcoming Ohio utility acquisition and pipeline expansions are expected to support earnings growth starting in fiscal 2027.

Bottom Line

National Fuel delivered a strong start to fiscal 2026 with:

- Double-digit adjusted EPS growth

- Rising natural gas production

- Stable regulated utility earnings

- Continued infrastructure expansion

Future growth will likely depend on natural gas prices, Appalachian production efficiency, and regulatory progress on pipeline and utility projects.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 4/29/2026 After close

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?