Latest dividend announcement

Parker-Hannifin Corporation has raised its quarterly cash dividend to $2.00 per share. The new dividend marks an 11.1% increase from the previous quarterly payment of $1.80 per share. The board declared the dividend on April 23, 2026. This payment will represent Parker-Hannifin’s 304th consecutive quarterly dividend.

Details of the dividend distribution

Shareholders of record on May 8, 2026, will receive the dividend on June 5, 2026. The stock will also trade ex-dividend on May 8. At the new quarterly rate, the annualized dividend rises to $8.00 per share. Based on the recent share price of $973.88, the forward dividend yield stands near 0.82%. This remains modest in absolute terms, but Parker-Hannifin’s appeal rests more on dividend growth and quality than on current income.

Relevant valuation metrics

Parker-Hannifin trades at a premium valuation. The market capitalization stands at about $122.92 billion, while enterprise value reaches roughly $132.37 billion. The shares trade at 35.5 times trailing earnings and 28.6 times forward earnings. The price-to-sales ratio sits at 6.0, and EV/EBITDA stands near 25.0. These multiples imply high expectations for margin durability, aerospace demand, industrial recovery, and acquisition execution.

The company generated $20.46 billion in sales and $3.54 billion in net income on a trailing basis. Profitability remains strong. Gross margin stands at 37.4%, operating margin at 21.4%, and net margin at 17.3%. Return on equity reaches 25.8%, while return on invested capital stands at 16.2%. These figures support the premium valuation, but they leave limited room for operational disappointment.

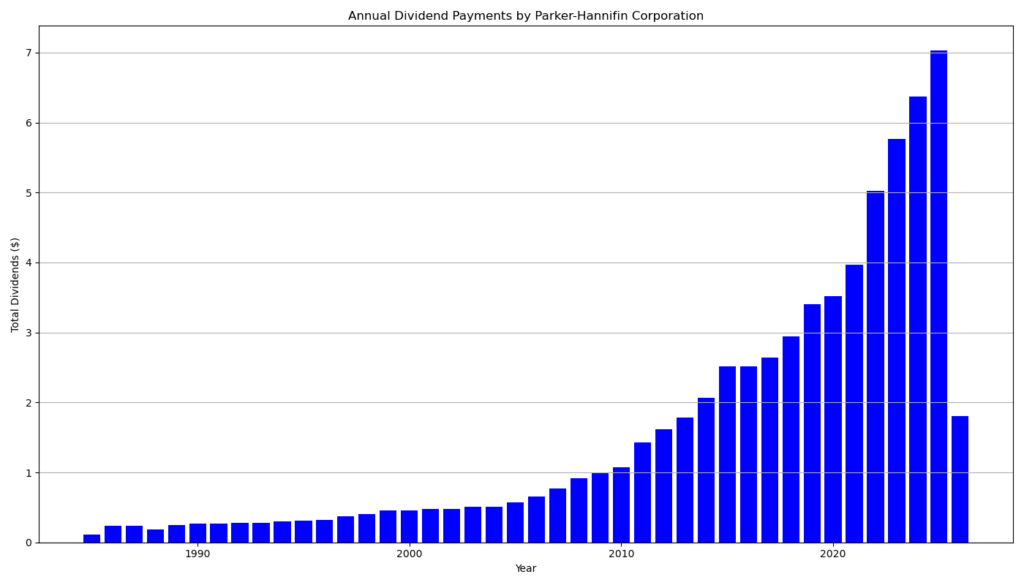

Dividend history and sustainability

The dividend increase extends Parker-Hannifin’s annual dividend growth record to 70 consecutive fiscal years. That places the company among the strongest dividend-growth names in the S&P 500. The latest increase also follows prior annual step-ups, including the move from $1.63 to $1.80 in 2025 and from $1.48 to $1.63 in 2024.

Dividend sustainability looks solid. The payout ratio stands near 24.7%, which gives management substantial flexibility. The new annual dividend of $8.00 remains well covered by trailing EPS of $27.42 and expected next-year EPS of $34.07. Cash generation also supports the distribution. In the first six months of fiscal 2026, Parker-Hannifin produced $1.64 billion in operating cash flow and paid $456 million in dividends.

Debt requires monitoring. Debt-to-equity stands at 0.69, with long-term debt-to-equity at 0.52. Parker-Hannifin also plans to acquire Filtration Group for about $9.25 billion in cash. This transaction could raise leverage, even though the company currently maintains an investment-grade profile.

Outlook for long-term investors

Parker-Hannifin offers a high-quality dividend-growth profile. The yield remains low, but the growth record, low payout ratio, and high returns on capital support long-term compounding. Investors should not ignore valuation risk. At more than 28 times forward earnings, the stock already prices in strong execution.

For long-term dividend investors, the shares suit a growth-and-quality strategy rather than a high-yield strategy. Future returns will depend on earnings growth, integration discipline, aerospace momentum, and continued margin resilience.

A brief company profile

Parker-Hannifin is a Cleveland-based global leader in motion and control technologies. The company serves aerospace, defense, industrial equipment, transportation, off-highway, energy, HVAC, and refrigeration markets. It employs about 57,950 people and operates through Diversified Industrial and Aerospace Systems. Its technology portfolio includes hydraulics, pneumatics, electromechanical systems, filtration, fluid handling, process control, engineered materials, and climate-control solutions.

last quarterly report*

Here is a concise summary of the latest quarterly report for Parker-Hannifin (Q2 FY2026, ended Dec 31, 2025):

Core Financial Performance

- Revenue: $5.17 billion (+9% YoY)

- Net income: $845 million (down from $949 million YoY)

- EPS (diluted): $6.60 (vs. $7.25 YoY)

Interpretation:

Top-line growth is solid, but profitability declined due to higher costs, lower other income, and increased expenses. Margin compression is visible despite revenue expansion.

Profitability & Margins

- Gross margin: ~37.3% (up from 36.3%)

- Net margin: ~16.3% (down from 20.0%)

Interpretation:

Operational efficiency improved (gross margin), but below-the-line factors (interest, taxes, lower gains) reduced net profitability.

Cash Flow & Capital Allocation

- Operating cash flow (6M): $1.64 billion

- Dividends paid (6M): $456 million

- Share buybacks (6M): $550 million

Interpretation:

Strong cash generation comfortably covers dividends. Additional capital is returned via buybacks, signaling shareholder-friendly allocation.

Balance Sheet & Debt

- Total assets: $30.5 billion

- Total debt (approx.): $9.9 billion (incl. short + long-term)

- Debt-to-equity ratio: ~0.41 (well below covenant limit)

Interpretation:

Leverage remains controlled. The balance sheet supports further acquisitions and continued dividend payments.

Dividend Profile

- Quarterly dividend: $1.80 per share

- 6M dividends per share: $3.60

- Dividend streak: 69 consecutive years of increases

Interpretation for dividend investors:

- Highly reliable dividend payer with exceptional track record

- Payout appears well covered by earnings and cash flow

- Long-term dividend growth credibility is strong

Growth Drivers & Segments

- Diversified Industrial revenue: $3.47B (+7% YoY)

- Aerospace Systems revenue: $1.71B (+15% YoY)

Interpretation:

Growth is broad-based, with aerospace as the stronger contributor. This mix supports margin expansion and long-cycle visibility.

Strategic Developments

- $1.0B acquisition of Curtis Instruments

- Planned $9.25B Filtration Group acquisition

Implication:

Aggressive M&A strategy may drive long-term growth but increases integration and financing risks.

Key Takeaways for Dividend Investors

- Strengths:

- Strong revenue growth and backlog (~$11.7B)

- Robust cash flow supports dividends

- Long dividend growth history (69 years)

- Risks:

- Declining net income and EPS

- Increasing acquisition-related leverage risk

- Margin pressure below operating level

Bottom Line

Parker-Hannifin remains a high-quality industrial dividend compounder. The current quarter shows operational strength but weaker bottom-line performance. Dividend safety is not in question, but near-term earnings pressure and acquisition execution will determine future dividend growth pace.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 4/30/2026 7:30 AM

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.