Latest dividend announcement

Toll Brothers has approved a quarterly cash dividend of $0.26 per share. The new payout is 4% above the prior quarterly dividend of $0.25, so the company did in fact raise the distribution from the previous period. The dividend is payable on April 24, 2026, to shareholders of record on April 10, 2026, with the stock trading ex-dividend on April 10. Management also stated that this marks the sixth consecutive year of dividend increases.

Details of the dividend distribution

On an annualized basis, the new dividend rate equals $1.04 per share. Based on the latest market price of about $143.24, the forward dividend yield is roughly 0.7% to 0.75%. That yield is modest, but Toll Brothers has positioned the dividend as a steadily growing capital-return tool rather than a high-yield income vehicle. For investors focused on dividend durability, the more important point is coverage. Using the company’s trailing EPS of about $13.92 and annualized dividend of $1.04, the earnings payout ratio sits near 7% to 8%, which is very conservative.

Relevant valuation metrics

Toll Brothers still screens as a low-multiple cyclical. At the current share price, the stock trades at about 10.3 times trailing earnings and roughly 10.0 times forward earnings. Price-to-book is around 1.6, which is reasonable for a builder that continues to earn solid margins and generate returns above its cost of capital. Enterprise value stands near $15.2 billion, with EV/EBITDA near 8.1. These metrics suggest that the market still applies a cyclical discount despite resilient profitability.

The latest quarter supports that valuation case. In fiscal first-quarter 2026, Toll Brothers reported net income of $210.9 million and diluted EPS of $2.19, up from $177.7 million and $1.75 a year earlier. Home sales revenue held essentially flat at $1.85 billion, while contract value rose to $2.38 billion. At quarter-end, the company held about $1.2 billion of cash against roughly $2.85 billion of total debt. That balance sheet strength gives management ample room to fund land investment, buy back stock, and continue growing the dividend.

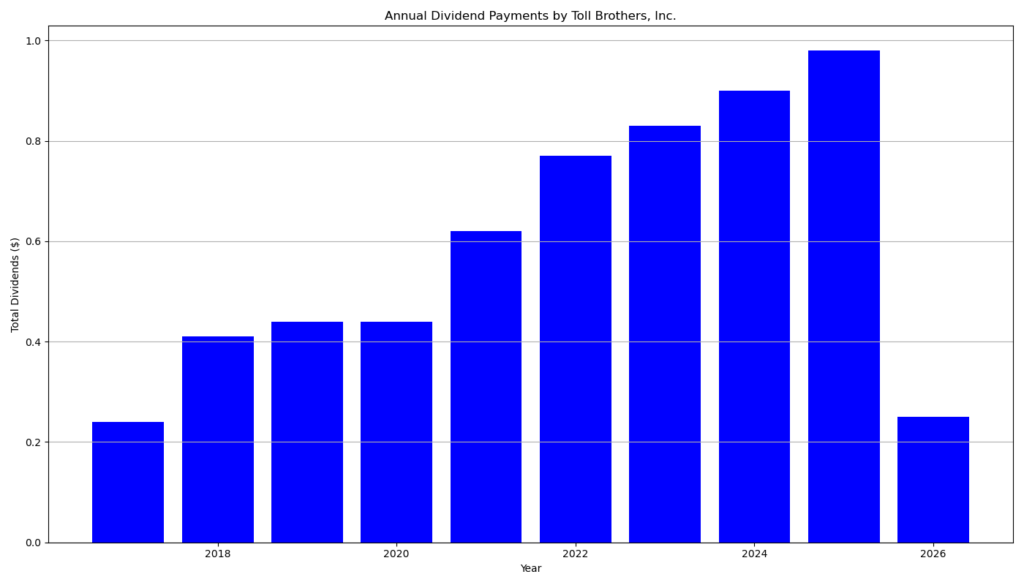

Dividend history and sustainability

The dividend history shows a consistent upward pattern, but not a rapid one. Toll Brothers paid $0.11 per quarter through much of 2019 and 2020, then raised the payout to $0.17 in 2021, $0.20 in 2022, $0.21 in 2023, $0.23 in 2024, $0.25 in 2025, and now $0.26 in 2026. That progression confirms steady annual growth rather than irregular jumps. It also supports the claim of six consecutive annual increases when the new March 2026 raise is included.

From a sustainability standpoint, the dividend looks secure. The payout ratio is low, free cash flow remains positive, and the company’s cash position adds another layer of protection. The main constraint is not dividend affordability but housing-cycle volatility. If orders weaken sharply, dividend growth could slow. A cut, however, looks unlikely under current operating conditions.

Outlook for long-term investors

Long-term dividend investors should view Toll Brothers as a dividend-growth name with cyclical exposure, not as a bond substitute. The yield is low, but the balance sheet is sound, earnings coverage is strong, and valuation remains undemanding. The key risk is macro sensitivity. Luxury housing demand can weaken when rates stay elevated, affordability tightens, or consumer confidence falls. Still, the company’s premium positioning, disciplined capital allocation, and conservative payout policy give it room to compound shareholder returns over time.

A brief company profile

Founded in 1967 and public since 1986, Toll Brothers is the leading U.S. luxury homebuilder. The company operates in more than 60 markets and also runs related businesses in architecture, engineering, mortgage, title, land development, smart-home technology, landscaping, and building products manufacturing. That integrated operating model helps support margins and strengthens its competitive position across the upscale housing market.

last quarterly report*

Toll Brothers posted a solid quarter, but the underlying picture is mixed. Revenue rose to $2.15 billion from $1.86 billion, and net income increased to $210.9 million from $177.7 million. Diluted EPS improved to $2.19 from $1.75. These gains came despite weaker delivery volume, helped by a higher average selling price and a large jump in land sales and other revenue.

For dividend investors, the key point is that profitability still grew. Higher earnings and EPS generally support dividend capacity. Toll Brothers also declared and paid a quarterly dividend of $0.25 per share during the quarter. The company noted that its credit agreements still allowed it to pay up to about $4.34 billion in cash dividends at January 31, 2026, so covenant pressure does not appear to be an immediate issue.

Operationally, the quarter was less straightforward. Home deliveries fell 5% to 1,899 units, but the average delivered price rose 6% to about $976,800. Net contracts signed by value increased 3% to $2.38 billion, while unit orders were essentially flat at 2,303 homes. That means Toll is still selling homes at strong price points, but volume momentum is not especially strong.

The backlog deserves a more critical reading. Backlog value fell 13% to $6.02 billion, and backlog units dropped 20% to 5,051 homes. Management explained that a larger mix of spec homes reduced quarter-end backlog because those homes are often sold and delivered within the same quarter. That explanation is plausible, but the decline still matters. For investors, backlog is an important forward indicator of future revenue visibility. A lower backlog means less built-in revenue support for upcoming quarters, even if spec-home turnover partly offsets that effect.

The balance sheet remains strong. Cash and cash equivalents were about $1.20 billion, stockholders’ equity was $8.41 billion, and debt to total capitalization stood at 0.24x. Toll also had about $2.20 billion of unused borrowing capacity under its revolving credit facility and no outstanding revolver borrowings. For dividend investors, this matters because low leverage and strong liquidity improve resilience during slower housing cycles.

There are also a few caution flags. SG&A rose 7%, home sales gross margin was nearly flat at 75.2% versus 75.0%, and the effective tax rate increased to 22.9% from 19.7%. In addition, some of the earnings improvement came from unconsolidated entities and other income rather than purely from stronger core homebuilding operations. That makes the quarter good, but not as clean as the headline profit growth suggests.

The regional picture was uneven. Pacific performed very strongly, with revenue up 37% and pretax income up 99%, while South and Mountain were weaker in several measures. That mix shift toward higher-priced regions helped pricing, but it may not be fully repeatable if demand softens.

Bottom line: Toll Brothers remains financially strong, profitable, and supportive of its dividend. For retail dividend investors, the most important positives are earnings growth, ample liquidity, modest leverage, and continued cash dividend payments. The main watch items are the sharp backlog decline, flat order units, and the fact that part of earnings growth came from non-core items rather than broad-based volume expansion. If you want, I can also turn this into a dividend-investor article in the style you used in your earlier prompts.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 5/19/2026 After close

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?