Latest dividend announcement

Comfort Systems USA, Inc. announced a quarterly dividend of $0.80 per share, representing a 14.3% increase from the previous payout of $0.70. The company will pay the dividend on May 26, 2026, to shareholders of record as of May 15, 2026, with the ex-dividend date also set for May 15. This marks a continuation of the company’s disciplined capital return strategy and reflects confidence in its cash flow trajectory.

Details of the dividend distribution

The new annualized dividend amounts to $3.20 per share, compared to a trailing twelve-month payout of $2.25. Despite the increase, the dividend yield remains modest at approximately 0.17%, driven by the stock’s strong price appreciation. The payout ratio stands at 6.75%, which indicates a conservative distribution policy and substantial retained earnings for reinvestment. The low payout ratio also provides significant headroom for future dividend increases without stressing liquidity.

Relevant valuation metrics

Comfort Systems reported Q1 2026 revenue of $2.87 billion, representing 56.5% year-over-year growth, and earnings per share of $10.51, significantly exceeding expectations. On a trailing basis, the company generates $10.14 billion in annual revenue and $1.22 billion in net income, reflecting strong operational leverage. Profitability metrics remain robust, with a net margin of 12.07%, return on equity of 53.29%, and return on invested capital of 38.80%.

Valuation remains demanding. The stock trades at a P/E ratio of 49.82 and a forward P/E of 35.69, indicating that the market prices in sustained high growth. The EV/EBITDA multiple of 34.57 and price-to-free-cash-flow ratio of 44.06 further confirm premium valuation levels. However, the balance sheet remains strong, with a debt-to-equity ratio of 0.13 and solid liquidity ratios above 1.2, supporting financial flexibility.

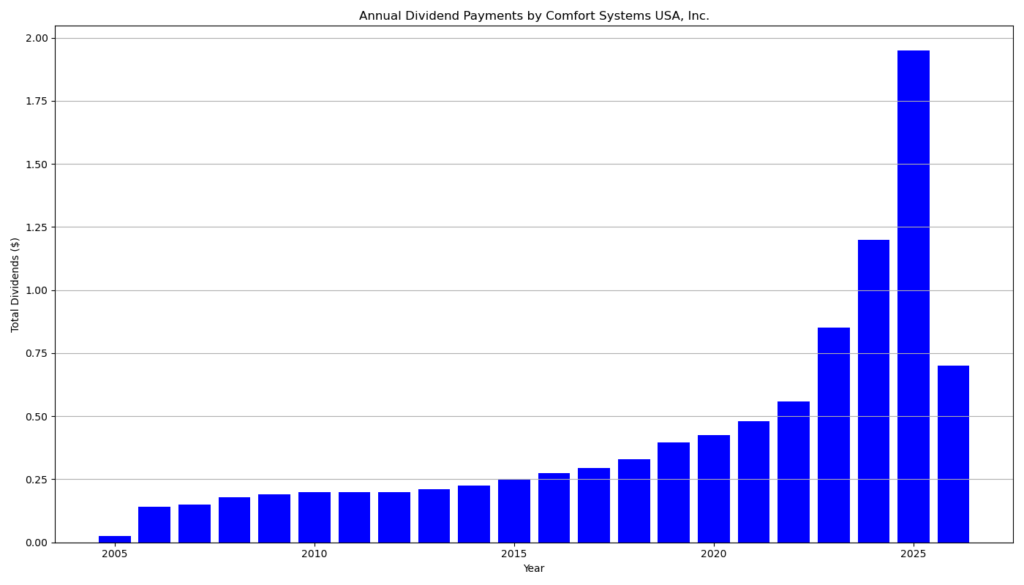

Dividend history and sustainability

Comfort Systems has established a consistent dividend growth profile. The company has delivered 13 consecutive years of dividend increases and 20 consecutive years of uninterrupted payments. The dividend has accelerated significantly in recent years. Quarterly payouts rose from $0.25 in early 2023 to $0.80 in 2026, reflecting rapid earnings expansion.

The three- and five-year dividend growth rates of 51.57% and 35.94%, respectively, indicate aggressive capital returns. However, this pace aligns with earnings growth, as EPS increased more than 100% year-over-year. The low payout ratio and high return metrics suggest that the dividend remains highly sustainable, even under more moderate growth assumptions.

Outlook for long-term investors

The investment case centers on growth rather than income. The current yield remains low, but the combination of high earnings growth, strong margins, and disciplined capital allocation supports continued dividend expansion. The company benefits from structural demand in HVAC, electrical, and infrastructure services, particularly in industrial and data center markets.

However, valuation risk is material. Elevated multiples leave limited margin for execution errors or cyclical downturns. Long-term investors should monitor margin stability, backlog conversion, and capital allocation discipline. Dividend growth remains credible, but future increases may normalize as the company scales.

A brief company profile

Comfort Systems USA operates as a leading provider of mechanical and electrical contracting services across the United States. The company maintains a network of nearly 200 locations in over 140 cities and serves commercial, industrial, and institutional clients. Its services include HVAC installation, maintenance, and integrated building systems. Since its IPO in 1997, the company has expanded through acquisitions and organic growth, positioning itself as a key player in building infrastructure and energy efficiency solutions.

last quarterly report*

Summary of Q1 2026 Results – Comfort Systems USA, Inc.

Comfort Systems USA, Inc. delivered exceptionally strong financial performance in the first quarter of 2026, driven by robust demand in technology and infrastructure markets.

Revenue and earnings growth

- Revenue increased to $2.87 billion, up 56.5% year-over-year

- Net income rose to $370.4 million, more than doubling from the prior year

- Diluted EPS reached $10.51, compared to $4.75 last year

Growth came primarily from strong same-store activity (over 50%), especially in data center and technology-related projects.

Profitability expansion

- Operating income increased to $485.7 million

- Operating margin improved to 17.0% (from 11.4%)

- Gross margin expanded to 26.3%, supported by improved project execution and favorable contract adjustments

Cash flow and balance sheet

- Operating cash flow reached $388.8 million, a major improvement from negative levels last year

- Free cash flow totaled $242.2 million

- Cash position increased to $1.05 billion

- Debt remains low at roughly $39 million, with no outstanding borrowings under the credit facility

→ This reflects strong liquidity and conservative leverage, important for dividend sustainability.

Backlog and demand visibility

- Total backlog reached $12.45 billion, up 80.8% year-over-year

- The majority relates to large-scale construction projects, particularly in technology infrastructure

→ This backlog provides short- to medium-term revenue visibility.

Operational drivers

- Mechanical segment: $2.06 billion revenue (+47%)

- Electrical segment: $804.7 million revenue (+87%)

- Growth concentrated in data centers, manufacturing, and industrial facilities

Dividend and capital allocation

- The company paid a $0.70 quarterly dividend in Q1

- Strong earnings and low payout ratio indicate substantial capacity for dividend growth

- Share repurchases remain limited but ongoing

Key takeaway for investors

Comfort Systems combines:

- High growth (revenue, EPS, backlog)

- Strong profitability and margins

- Robust cash generation and low debt

However, the business remains cyclical and tied to construction demand, and recent performance reflects an unusually strong macro environment. Sustainability depends on continued investment in infrastructure and technology sectors.

Conclusion

Q1 2026 confirms that Comfort Systems operates at a high-growth, high-return profile with strong financial discipline. The company currently prioritizes reinvestment and expansion, while maintaining a conservative but rapidly growing dividend base.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 7/23/2026 After close

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.