Latest dividend announcement

Goldman Sachs has declared a quarterly common dividend of $4.50 per share. The dividend is payable on June 29, 2026, to shareholders of record on June 1, 2026, with the ex-dividend date also set for June 1, 2026. This announcement does not mark a new increase. The payout remains unchanged from the prior quarter’s $4.50 distribution. The last increase occurred in the payout declared for the March 2026 payment, when Goldman lifted the quarterly dividend from $4.00 to $4.50, a 12.5% step-up. Goldman disclosed the new declaration in its first-quarter 2026 earnings release.

Details of the dividend distribution

At the current run rate, Goldman Sachs now pays an annualized dividend of $18.00 per share. Based on the share price provided, that implies a forward dividend yield of roughly 2.0%, which aligns with the market data in the prompt. The stock’s trailing twelve-month dividend of $15.50 shows that the latest annualized run rate still reflects the late-2025 increase rather than a fresh move this quarter. Goldman returned $6.38 billion to common shareholders in the first quarter of 2026, including $5.00 billion in buybacks and $1.38 billion in common dividends. That capital return mix matters. Goldman still favors repurchases as its primary distribution lever, while the dividend serves as the stable base layer.

Relevant valuation metrics

For long-term dividend investors, Goldman’s key metrics look solid. The stock trades at about 16.6 times trailing earnings and 14.0 times forward earnings, which suggests the market still prices in cyclical earnings risk despite a strong franchise. The price-to-book ratio of 2.51 is elevated versus the bank’s own historical trough multiples, but it also reflects improved profitability and better business mix. Book value per share stands at $361.91, and Goldman reported first-quarter 2026 diluted EPS of $17.55, net earnings of $5.63 billion, revenue of $17.23 billion, and ROE of 19.8%. The stated payout ratio of 27.28% remains conservative. That low earnings payout gives Goldman ample dividend coverage even if capital markets activity cools.

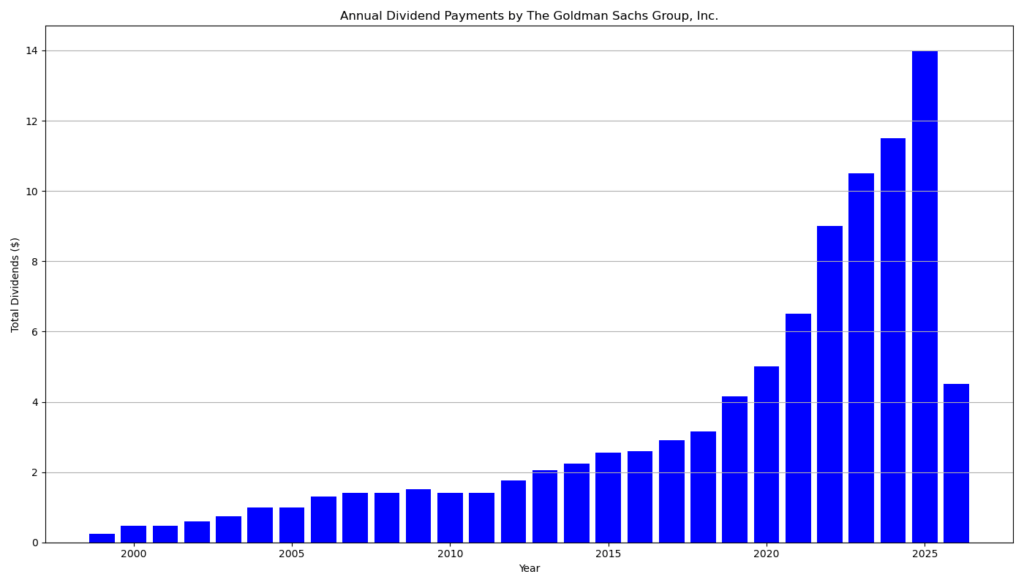

Dividend history and sustainability

Goldman’s dividend record looks credible, but investors should keep the history in context. The company has paid dividends for 26 consecutive years and has delivered 14 consecutive years of dividend growth according to the data provided in the prompt. The growth path has not been linear. Goldman cut its dividend during the financial crisis, then rebuilt it gradually. More recently, the quarterly payout moved from $2.50 in 2023 to $3.00 in 2024, then to $4.00 and $4.50 in 2025 and early 2026. That pattern shows disciplined but uneven growth tied to earnings power, regulatory capital, and board confidence. Sustainability looks strong because the cash commitment is modest relative to earnings, and Goldman still generated robust capital returns in the latest quarter. However, investors should monitor capital ratios. The firm’s CET1 ratio fell to 12.5% from 14.3% at year-end 2025, which reduces part of the cushion, even though the ratio remains above regulatory minimums. Broader U.S. capital-rule revisions could later improve flexibility for shareholder distributions.

Outlook for long-term investors

Goldman Sachs fits best as a total-return bank rather than a pure income vehicle. The dividend is well covered, the payout ratio is low, and buybacks remain material. That combination supports long-term compounding. Still, the earnings base is cyclical. Investment banking, trading, and market sentiment can swing sharply across quarters. Dividend investors should therefore focus less on headline yield and more on Goldman’s ability to sustain high returns on equity, grow book value, and preserve capital through the cycle. On that basis, the current dividend appears secure, but future growth will likely remain episodic rather than mechanical.

A brief company profile

Goldman Sachs is a global financial institution headquartered in New York. It operates across investment banking, global markets, and asset and wealth management. The company is a constituent of the Dow Jones Industrial Average and the S&P 500, employs about 47,400 people, and continues to combine advisory, trading, financing, and investment management under one platform. That diversified model gives Goldman multiple earnings engines, but it also keeps the stock tied to the broader capital-markets cycle.

last quarterly report*

Goldman Sachs – Q1 2026 Results Summary (Dividend-Focused)

Core Financial Performance

- Net revenue: $17.23 billion (+14% YoY)

- Net earnings: $5.63 billion (+19% YoY)

- EPS (diluted): $17.55 (+24% YoY)

- ROE: 19.8% (strong profitability)

Interpretation:

Goldman delivered a strong quarter with double-digit growth across revenue, earnings, and EPS. The nearly 20% ROE indicates efficient capital allocation—critical for sustaining shareholder returns.

Segment Drivers

- Global Banking & Markets: $12.74 billion (+19% YoY)

- Investment banking fees +48% (M&A rebound)

- Equities +27% (strong trading and financing)

- FICC ‑10% (weaker fixed income activity)

- Asset & Wealth Management: $4.08 billion (+10% YoY)

- Growth driven by higher assets under supervision

- Platform Solutions: $411 million (decline YoY due to loan portfolio markdowns)

Interpretation:

Revenue growth is cyclical and heavily tied to capital markets activity. The rebound in investment banking is positive but not structurally stable.

Costs and Efficiency

- Operating expenses: $10.43 billion (+14% YoY)

- Efficiency ratio: 60.5% (flat YoY)

Interpretation:

Costs increased in line with revenue. No meaningful operating leverage improvement.

Balance Sheet & Risk

- Total assets: $2.06 trillion

- CET1 ratio: 12.5% (down from 14.3%)

- Supplementary leverage ratio: 4.6% (declining)

Interpretation:

Capital ratios declined. Still adequate, but the trend is negative and relevant for dividend capacity under regulatory constraints.

Cash Returns to Shareholders

- Dividend: $4.50 per share (quarterly)

- Total dividends paid: $1.38 billion

- Share buybacks: $5.00 billion

- Total capital return: $6.38 billion

Interpretation:

Goldman prioritizes buybacks over dividends. The dividend is stable but not the primary capital return mechanism.

Dividend Analysis

- With EPS of $17.55, the quarterly dividend of $4.50 implies:

- Payout ratio ≈ 26%

Interpretation:

- Low payout ratio → high safety margin

- Significant capacity for future increases

- However, management prefers flexible buybacks over committing to higher dividends

Key Takeaways for Dividend Investors

- Strong earnings power supports dividend sustainability.

- Low payout ratio indicates the dividend is very safe.

- Capital returns skewed toward buybacks, not income.

- Cyclical revenue base (investment banking, trading) introduces volatility.

- Declining capital ratios should be monitored for regulatory pressure.

Bottom Line

Goldman Sachs offers a secure but modest dividend profile. It is not a pure income stock. The investment case rests more on total shareholder return (buybacks + growth) than on consistent dividend growth.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 7/14/2026 7:30 AM

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.