Latest dividend announcement

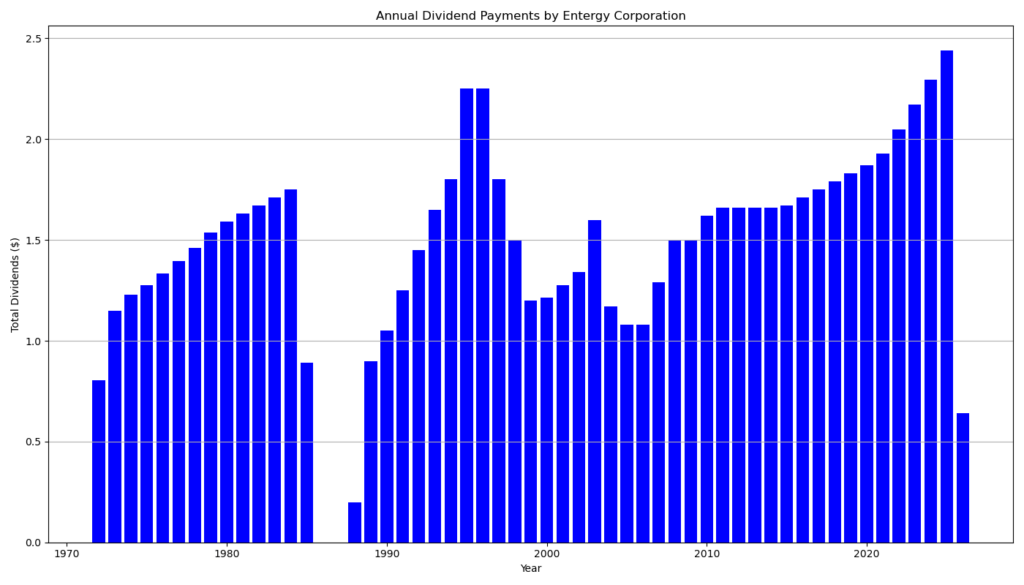

Entergy has declared a quarterly dividend of $0.64 per share. The payout is unchanged from the previous quarter. That is the correct framing here: the board did not increase the dividend in April. The company has now declared the same $0.64 quarterly rate for three consecutive quarters. The dividend is payable on June 1, 2026, to shareholders of record on May 1, 2026, with the stock trading ex-dividend on May 1.

Details of the dividend distribution

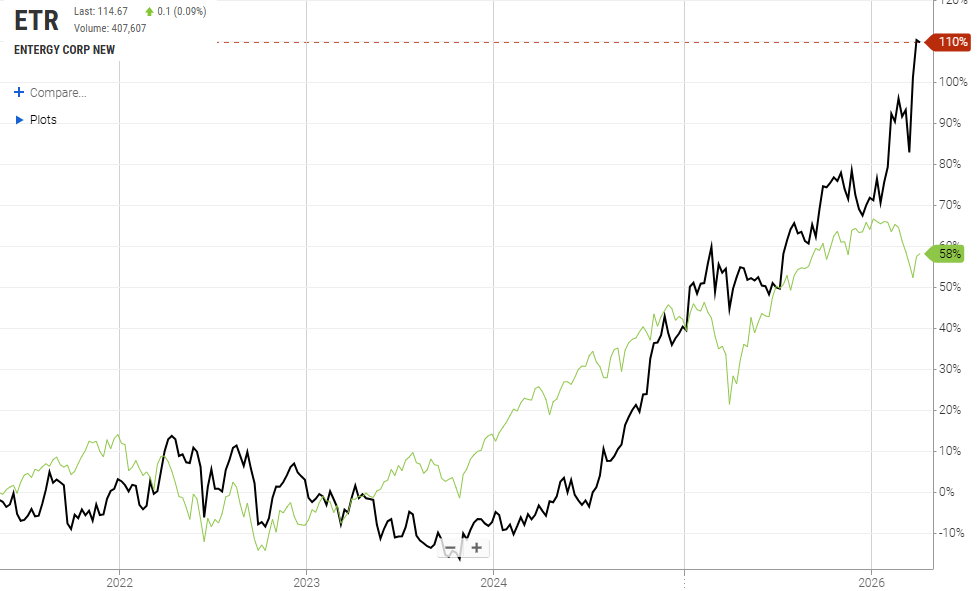

At the current quarterly rate, Entergy’s annualized dividend stands at $2.56 per share. Based on the recent share price around $115, that implies a forward yield of roughly 2.2%, which aligns with the market data provided. The last actual increase came in late 2025, when Entergy lifted the quarterly dividend from $0.60 to $0.64. That was a 6.7% increase. Before that move, the company had held the payout at $0.60 for four straight quarters.

Relevant valuation metrics

For dividend investors, the valuation setup looks reasonable rather than cheap. The supplied market data shows a trailing P/E of 29.4 and a forward P/E of 23.3. That gap matters because it reflects expected earnings growth rather than multiple expansion alone. Entergy reported 2025 adjusted EPS of $3.91 and issued 2026 adjusted EPS guidance of $4.25 to $4.45. On that basis, the current dividend implies a trailing payout ratio of about 65.5% and a forward payout ratio of roughly 58% to 60%. Those figures sit in a manageable range for a regulated utility with visible cash generation. Entergy also generated $5.15 billion in operating cash flow in 2025, delivered adjusted ROE of 11.0%, and improved FFO-to-adjusted debt to 17.2%.

Dividend history and sustainability

The recent dividend profile is constructive, but the long-term history needs context. Entergy has paid a cash dividend continuously since 1988. However, it does not have a clean multi-decade dividend growth streak. The historical record includes cuts in earlier periods, including 2004 and 1998. That means investors should treat Entergy as a reliable payer, not as a classic uninterrupted dividend-growth compounder. More recently, the pattern has improved. After the 2‑for‑1 stock split that took effect in December 2024, the dividend history shows a steady climb from a split-adjusted $0.565 to $0.60 and then to $0.64. The supplied growth figures of about 6.0% over three years and 5.5% over five years fit that recent cadence.

Outlook for long-term investors

The investment case rests on regulated rate-base growth, rising industrial demand, and improving earnings visibility. Entergy’s 2025 results showed full-year EPS growth, stronger operating cash flow, and weather-adjusted retail sales growth of 3.9%, led by a 6.7% increase in industrial volume. Management also highlighted expanding demand from data centers and other large customers. The main constraint is leverage. Total debt ended 2025 at $31.1 billion, and interest expense remains a material drag. Still, the combination of a mid-single-digit dividend growth profile, a moderate payout ratio, and regulated utility cash flows supports a stable long-term income case.

A brief company profile

Entergy is a regulated electric utility and power infrastructure company serving more than 3 million customers across Arkansas, Louisiana, Mississippi, and Texas. The group operates generation, transmission, and distribution assets and continues to invest in grid resilience, modern natural gas, nuclear generation, and renewables. That asset mix gives the company a defensible earnings base and makes the stock relevant for long-term investors who prioritize dividend stability over headline yield.

last quarterly report*

Entergy (ETR) – 2025 Earnings Summary

Core financial performance

- Full-year EPS: $3.91 (vs. $2.45 in 2024 reported; $3.65 adjusted) → strong year-over-year growth

- Q4 EPS: $0.51 (vs. $0.65 in Q4 2024) → quarterly decline despite strong full-year results

- Net income (FY 2025): ~$1.76 billion (vs. ~$1.06 billion in 2024)

Interpretation:

Full-year earnings growth was robust, but the weaker Q4 suggests rising cost pressure and interest burden.

Key drivers of earnings

- Positive:

- Regulatory approvals and rate actions

- Higher electricity demand (especially industrial)

- Increased returns on infrastructure investments

- Lower nuclear outage costs

- Negative:

- Higher interest expense

- Rising O&M costs (maintenance, bad debt, outages)

- Higher depreciation and taxes

Interpretation:

Growth is driven by regulated asset expansion, but cost inflation and financing costs are becoming material headwinds.

Cash flow and balance sheet

- Operating cash flow: ~$5.15 billion (up from ~$4.49 billion)

- Total debt: ~$31.1 billion (increased YoY)

- FFO-to-debt: 17.2% (improved from 14.7%)

- Liquidity: Strong, with ~$7.9 billion net liquidity

Interpretation (dividend relevance):

- Strong cash flow supports dividend sustainability

- However, rising leverage and interest costs need monitoring

Return metrics

- ROE: 11.0% (vs. 7.1% in 2024)

Interpretation:

Solid improvement reflects effective rate base growth and regulatory outcomes—positive for long-term dividend capacity.

Operational trends

- Retail electricity sales (weather-adjusted): +3.9%

- Industrial demand: +6.7% (key growth driver)

Interpretation:

Demand growth—especially from industrial and data center customers—is a structural tailwind.

Guidance

- 2026 EPS guidance: $4.25–$4.45

Interpretation:

Implies continued earnings growth (~9–14%), supporting future dividend increases.

Overall assessment (dividend investor perspective)

- Strengths:

- Stable regulated utility model

- Strong cash flow generation

- Improving ROE and earnings growth

- Visible demand growth (industrial + data centers)

- Risks:

- Rising debt and interest costs

- Increasing operating expenses

- Capital-intensive growth strategy

Conclusion:

Entergy shows solid earnings and cash flow growth with supportive long-term demand trends. The dividend outlook appears stable to growing, but balance sheet leverage and cost inflation warrant close monitoring.

*This is the latest quarterly report that the company has filed with the SEC.

Next Earnings Date: 4/28/2026 6:00 AM

Die Selektion dieser Aktie erfolgte zufällig aus einem breiten Spektrum an tagesaktuellen Börsenmitteilungen bezüglich angekündigter Dividendenzahlungen. Der vorliegende Beitrag zielt nicht auf eine qualitative Bewertung dieser dividendenstarken Aktie ab, sondern verfolgt einen rein deskriptiven Ansatz.

Was sind Dividend Champions, Contenders, Challengers?

Disclaimer: Dieser Bericht dient ausschließlich Informationszwecken und stellt keine Anlageberatung oder Empfehlung zum Kauf oder Verkauf von Wertpapieren dar. Für die Richtigkeit der Daten wird keine Gewähr übernommen.